The concept of quality costs is a means to quantify the total cost of quality-related efforts and deficiencies. It was first described by Armand V. Feigenbaum in a 1956 Harvard Business Review article.

Prior to its introduction, the general perception was that higher quality requires higher costs, either by buying better materials or machines or by hiring more labor. Furthermore, while cost accounting had evolved to categorize financial transactions into revenues, expenses, and changes in shareholder equity, it had not attempted to categorize costs relevant to quality. By classifying quality-related entries from a company's general ledger, management and quality practitioners can evaluate investments in quality based on cost improvement and profit enhancement.

Feigenbaum defined the following quality cost areas:

The central theme of quality improvement is that larger investments in prevention drive even larger savings in quality-related failures and appraisal efforts. Feigenbaum's categorization allows the organization to verify this for itself. When confronted with mounting numbers of defects, organizations typically react by throwing more and more people into inspection roles. But inspection is never completely effective, so appraisal costs stay high as long as the failure costs stay high. The only way out of the predicament is to establish the "right" amount of prevention.

Once categorized, quality costs can serve as a means to measure, analyze, budget, and predict.

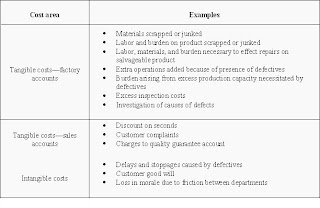

Variants of the concept of quality costs include cost of poor quality and categorization based on account type, described by Joseph M. Juran:

Cost of Poor Quality

Cost of poor quality (COPQ) or poor quality costs (PQC), are defined as costs that would disappear if systems, processes, and products were perfect.

COPQ was popularized by IBM quality expert H. James Harrington in his 1987 book Poor Quality Costs. COPQ is a refinement of the concept of quality costs. In the 1960s, IBM undertook an effort to study its own quality costs and tailored the concept for its own use. While Feigenbaum's term "quality costs" is technically accurate, it's easy for the uninitiated to jump to the conclusion that better quality products cost more to produce. Harrington adopted the name "poor quality costs" to emphasize the belief that investment in detection and prevention of product failures is more than offset by the savings in reductions in product failures.

COPQ decomposes COPQ into the following elements:

Example:

White collar COPQ:

Harrington noted that expanding cost analyses to management and clerical workers could also make a significant dent in waste. He defined the following costs by functional area:

Highest Quality is Lowest Cost

Highest quality is lowest cost" is a Japanese manufacturing aphorism based on the premise that the highest quality manufacturer will earn a reputation that makes buyers prefer, price being reasonably similar, to buy its goods. This means that the manufacturer will produce more than its competitors, and thus will both have economies of scale and be able to accept a lower profit per unit—thus the highest quality goods will have a lower cost by driving other goods from the market. The production of higher quality goods can also reduce quality costs.

Cost of Poor Quality

Cost of poor quality (COPQ) or poor quality costs (PQC), are defined as costs that would disappear if systems, processes, and products were perfect.

COPQ was popularized by IBM quality expert H. James Harrington in his 1987 book Poor Quality Costs. COPQ is a refinement of the concept of quality costs. In the 1960s, IBM undertook an effort to study its own quality costs and tailored the concept for its own use. While Feigenbaum's term "quality costs" is technically accurate, it's easy for the uninitiated to jump to the conclusion that better quality products cost more to produce. Harrington adopted the name "poor quality costs" to emphasize the belief that investment in detection and prevention of product failures is more than offset by the savings in reductions in product failures.

COPQ decomposes COPQ into the following elements:

Example:

White collar COPQ:

Harrington noted that expanding cost analyses to management and clerical workers could also make a significant dent in waste. He defined the following costs by functional area:

Highest Quality is Lowest Cost

Highest quality is lowest cost" is a Japanese manufacturing aphorism based on the premise that the highest quality manufacturer will earn a reputation that makes buyers prefer, price being reasonably similar, to buy its goods. This means that the manufacturer will produce more than its competitors, and thus will both have economies of scale and be able to accept a lower profit per unit—thus the highest quality goods will have a lower cost by driving other goods from the market. The production of higher quality goods can also reduce quality costs.

From the purchaser's point of view the highest quality goods will have the fewest problems, and the cost of dealing with a problem far outweighs the extra purchase cost.

I have added Quality World into my blog.

ReplyDeleteWould you please also refer to my blog at http://qualityalchemist.blogspot.com ?